Economic Forecast 2022

Most contractors and subcontractors are looking back at a better-than-expected 2021. After the bottom fell out in the first half of 2020 when coronavirus-related shutdowns stalled the nation, the economy came roaring back in the second half with enough demand—driven mainly by consumer spending—to carry over into 2021.

The coronavirus spurred new housing starts; many workers, suddenly gone virtual and untethered from their physical workplaces, saw the opportunity to re-locate and took it. Many city dwellers suddenly denied access to the things they lived in cities for (restaurants, sporting events, entertainment venues, high-rise office buildings) decided to give suburban or even rural living a try. Many who didn’t relocate still decided to invest in making their baths and kitchens—places they reasoned they’d be spending a lot more time in—more comfortable, giving a boost to the remodeling market.

But now, as the country starts in on its third year of the pandemic, most of that pent-up demand has been met.

While growth will continue in 2022—and while another recession seems unlikely—the rate of growth will most likely decrease.

Here are a few key indicators that support that view, followed by a few “wild cards” to keep in mind as we start 2022.

GDP

According to the Bureau of Economic Analysis (www.bea.gov), real gross domestic product (GDP) increased at an annual rate of 2.3 percent in the third quarter of 2021, following an increase of 6.7 percent in the second quarter. The increase was revised up 0.2 percentage point from the “second” estimate released in November. This deceleration in real GDP in the third quarter was led by a slowdown in consumer spending.

Also in the third quarter, government assistance payments in the form of forgivable loans to businesses, grants to state and local governments, and social benefits to households all decreased, a tapering off from assistance programs that were pushed out during the initial phase of the pandemic. With the current resurgence of cases thanks to the new Omicron variant, it remains to be seen if this assistance will be ramped back up.

According to investment firm Goldman Sachs, the firm now sees 2022 gross domestic product (GDP) growth of 3.8%, down from 4.2% previously on a full year basis, and Q4/Q4 growth of 2.9%, down from 3.3% before. Most of the predicted deceleration is, again, due to concerns around the coronavirus and its new variants.

Inflation

Annual inflation rate in the US accelerated to 6.8% in November of 2021, the highest since June of 1982, and in line with forecasts. It marks the 9th consecutive month the inflation stays above the Fed's 2% target. Some of the reasons for increase included a rally in global commodities, rising demand, wage pressures, and supply chain disruptions.

Projections from mortgage lender Fannie Mae have inflation averaging 7.0 percent in Q1 2022 before decelerating to 3.8 percent by the end of 2022.

Keep in mind, a certain amount of inflation is already “priced into” the economy. Also, if wages are keeping pace with inflation, it blunts the effect of rising prices. Inflation can also motivate consumers to buy and invest NOW, rather than wait for time to rob their money of value.

The classic method of dealing with rising inflation is through monetary policy. Fannie Mae expects 25 basis point Fed interest rate hikes in the second and fourth quarters of 2022 and continuing quarterly through 2023. There may be more aggressive tightening if inflation fails to decelerate in coming months due to supply chain issues taking longer to resolve, consumer spending remaining more robust, or if energy prices spike. More expensive loans may make consumers less likely to purchase—but the immediate prospect of more expensive loans, again, may push them to make that purchase sooner, rather than later.

Residential Construction

This jibes closely with information from the National Association of Home Builders. As of November (and due mainly to supply-chain effects) there are 152,000 single-family units authorized but not started construction—up 40.7% from a year ago. The reason for not starting? Supply chain constraints.

In December, single-family builder confidence increased one point to a level 84 (after a three point gain in November) on strong buyer demand, according to the NAHB/Wells Fargo Housing Market Index (HMI). After peaking at a level of 90 in November 2021, builders have reported ongoing concerns over elevated lumber and other construction costs, as well as delays in obtaining building materials.

Commercial Construction

In early January, Associated Builders and Contractors reported that National nonresidential construction spending was virtually unchanged in November month-over-month, according to an analysis of data published by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $820.6 billion for the month.

“While the monthly data is overall not jarring, the year-over-year numbers are more noteworthy,” said ABC Chief Economist Anirban Basu. “After declining during much of the pandemic, spending in the office segment has stabilized and is up 3.3% from a year ago. That may reflect data center construction spending more than traditional office space construction, however.”

With business travel still slow to return the lodging and hospitality sector will remain subpar for months to come. The nonresidential construction category experiencing the largest year-over-year growth in spending is manufacturing, a reflection of the ongoing efforts of producers to expand supply to meet demand. That growth is expected to carry over into 2022.

The Supply Chain

According to the latest data from the American Supply Association, supply chain flows have started to improve for some sectors, but there is still a tremendous backlog to work through. There are still nearly two million containers still headed inbound into the United States, which will help replenish inventories in some sectors (those without chronic raw material shortages).

Steel, particularly supplies of carbon steel pipe, has been in limited supply. Hot-rolled coil prices have fallen 12% in the last month, 20% off its one-year high, and lead times have returned to their historical norms. Carbon steel pipe prices are still holding firm, but the ASA anticipates prices to decline soon. In general, bearish sentiments are prevalent in the carbon steel market.

President Biden agreed to allow the UK to import more than 3 million annual tons of steel tariff-free. Japan and Korea have asked for a similar allowance. Increasing steel imports could help lower costs but may cost U.S. jobs.

As for iron, Tyler and Charlotte Pipe, the two leading domestic producers of cast-iron pipe and fittings, have settled on list price increases beginning in January 2022; superseding September, 2021 list pricing. No-hub coupling prices have remained stable since Sept. of 2021.

Thermoplastic PVF manufacturers are still seeing rolling product and pricing disruptions heading into 2022. The pace of price increases has slowed as resin plants push to catch up to market demand. Facilities damaged during winter storms in Texas back in February are largely back to fully operational. Global shipping and raw material supply concerns will continue to stress product availability forecasts.

CPVC pipe and fittings realized a 5%-10% increase in late Q4 2021 related to raw material availability tied to shipping delays. PVC will likely see an increase in early Q1 related to the availability of critical additives.

For more information and updates on prices throughout the year, visit the ASA web site at www.asa.net.

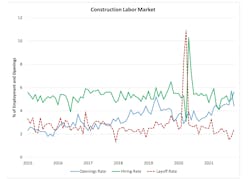

The Labor Market

Despite some narratives attributing the mass exodus to Millennials or Gen Z, it is the Baby Boomers that are having the largest impact on the numbers. In 2021, more than five million people over the age of 55 exited the labor force, with about 1.5 million of those choosing to take early retirement.

Hiring in the construction sector remained solid in November, rising to a 5.6% growth rate. Quits in the construction sector (as reported to the Bureau of the Labor) increased somewhat in construction, rising to 207,000 in November, a data series high.

As difficult as finding and hiring has been in the past decade, 2022 promises to be even more challenging. If there is a silver lining, it’s an influx of young people without four-year college degrees into the labor market who have decided to try something better for themselves and their careers than working retail, hospitality or food service.

Federal Regulation

With the passage of the Infrastructure Investment and Jobs Act in November, record amounts of money will be spent in the coming years on plumbing products and services. That including over $55 billion to expand access to clean drinking water through new infrastructure and to remove lead service lines. While the bidding process alone may take up all of 2022, many plumbing contractors, large and small, are in position to take on some of that new work.

At the same time, legislation at the state and federal level is, on the one hand, incentivizing alternative energy systems (geothermal and solar), and de-incentivizing fossil fuels such as natural gas. Some areas of California and New York have already outlawed the installation of natural gas appliances (which includes water heaters) in new construction.

The push towards electrification is all part of overall efforts to control CO2 emissions. Expect heat pump systems in particular, and high-efficiency system of all kinds, to see various incentives and subsidies in 2022 and the years ahead.

The Unexpected

At the time of this writing, hospitalization rates in most states are setting records thanks to the new Omicron variant of the coronavirus. At the same time, death rates have either plateaued or declined. Data from the latest wave of infections show the vaccines have been effective in limiting both the spread of the virus and mitigating the worst of its symptoms.

The unexpected emergence of the new variant combined with its rapid spread has caused a new wave of uncertainty as to what the future will hold, and what the response of elected officials will be. Still, world financial markets seem stable, many posting record highs.

Other areas of concern include foreign affairs. China has shown a new belligerence in the South Pacific and has kept a heavy hand on dissidents in the run-up to the Winter Olympics. North Korea is preparing a new ballistic missile test. Russia appears determined to invade the Ukraine. Any of these could lead to a downturn in the market and possible disruptions to the supply chain.

Domestically, the country remains sharply divided politically. 2022 is a midterm election year, and it looks very likely the Republicans will retake the House. Whether or not this sparks serious violent confrontation—and whether that reaches a level that affects the day-to-day operation of business—is anyone’s guess.

The best advice for the coming year was probably given by keynote speaker Conner Lokar at this year’s PHCC Connect: “Take a good hard look at your markets and decide if they are heading for a soft landing or a hard landing. Stay on top of aging receivables. Revisit capital expenditure plans.”