Life insurance policies: a victory or not?

My law school professor, who taught advanced estate planning, often said, "Life insurance, properly structured, in estate planning is the bedrock of beating up the IRS … legally." This article, based on my 50-plus years of experience, shows you why and how my old professor was then and, even today, is right.

Unfortunately, my experience with real-life clients also reveals that blunders involving life insurance cause more dollars to be lost to the IRS (and the heirs of these clients) than any other area in the income tax or estate tax. This is sad and, as you will see, unnecessarily so.

Why is life insurance such a powerful weapon (strategy) to enrich our clients at the expense of the IRS? Because the Internal Revenue Code is very kind to every aspect of life insurance. And why is no mystery because the insurance industry is very kind to the Washington politicians that keep the tax law favorable. Unfortunately, the law is complex and if you don't use the law properly, it will eat your lunch.

The rest of this article will show you how to take advantage of the law — no blunders. Actually, when you know how, it's easy.

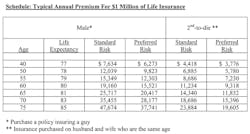

Let's start by examining the very important, but little-known economics of life insurance. The following schedule shows you the typical annual premium amount to buy a new (universal life) insurance policy with a $1 million death benefit.

Take a look at the Schedule to find your age (or close to your age). Three facts jump out at you:

Premiums become significantly higher as you age, so invest in life insurance as soon as you can afford it.

It pays to be healthy. "Preferred Risk" males get about a 20% discount compared to "Standard Risk" males.

Second-to-die insurance is a true bargain, receiving about a 40% discount and rising as you get older to over 50% at age 75.

NOTE: If you are healthy (for your age) life insurance works to about age 83 for males, 86 for females and age 88 for second-to-die. Remember, female life expectancy is three to four years more than a male who is the same age, thus lowering female premiums. Health normally declines with age and may put insurance out of range. Simply put, the insurance companies do not want your money unless they think you are going to live.

One significant fact (really a question) does not jump out at you when studying the schedule: How does the insurance company make money?

For example, let's take a 60-year-old male (Max), rated a standard risk with a 20-year life expectancy to age 80. In 20 years, Max will have paid only $383,200 ($19,160 x 20). Sure looks like the insurance company will on average (people living to life expectancy) take a big hit.

Not so fast. Here's another fact: Every year, continuing studies show that about 90% of so-called "permanent life insurance policies" (like universal life) do not pay a death benefit. Nice business model: Collect premiums year-after-year and then your customer decides to cancel his/her policy. Then, the insurance company is off of the death benefit hook. Please note that if you don't intend to keep the policy to the day you die, don't buy it in the first place.

Next, let's take a look at how the friendly tax laws work to make life insurance a tax-advantaged investment to multiply your wealth without risk.

Let's use Max as an example. If he lives to age 81 (one year past life expectancy), his premiums would total about $400,000 (rounded). With a $1 million death benefit Max’s profit is $600,000 and every penny is income tax-free. Thank you, tax law.

What about the estate tax? There are many ways to escape the estate tax (currently at a 35% rate, scheduled to go to a top rate of 55% in 2013). In Max's case we put the insurance into an "irrevocable life insurance trust" (ILIT) and all of the $1 million will escape the estate tax.

We have learned that real-life examples are the best way to teach how to get a life insurance victory and avoid blunders. My files are bulging with such examples. Following are five examples that come up often with real-life clients. As you read the examples, pick out the one (or more) that fits your personal circumstances. You'll see how easy it is to avoid losing tax dollars to the IRS or increase your wealth (tax-free) … always without risk.

Example No. 1: Insurance-funded buy/sell agreements.

Warren (56) and his brother Bill (58) have an insurance-funded buy/sell agreement. Both are in excellent health. An audit of the policies showed that Bill's policy would lapse at age 70 and Warren's at age 69. My insurance guru was able to arrange for a tax-free exchange for each brother, so the policies would be guaranteed to pay the death benefits ($2.1 million for each) no matter how long Warren or Bill might live (without any added premium cost). Nice!

CAUTION: It is rare that we find insurance-funded buy/sell agreements properly done. There are dozens of possibilities for expensive blunders — tax and otherwise (as above). Always get a second opinion.

Example No. 2: Life insurance no longer needed on husband.

Cal (59) and Cindy (55) are married. Cal's insurance consists of a death benefit of $788,000; cash surrender value (CSV) of $213,000; and an annual premium of $9,000. They are worth more than $9.5 million (mostly cash or cash-like investments). Cal earns more each year than they spend: so they don't really need single life insurance on Cal.

My network insurance consultant was able to use the $213,000 CSV, continuing the $9,000 annual premium to purchase a second-to-die policy with a $1.6 million death benefit … almost double the amount of old insurance. Powerful!

Example No. 3: Using life insurance as a tax-advantaged investment.

Wendy, a 76-year-old widow, is worth more than $12 million, mostly liquid investments. Her investment income far exceeds her lifestyle costs. Following is a wealth-increasing, two-step strategy.

First, Wendy paid $2 million for a single premium immediate annuity (means the insurance company will pay Wendy the same annuity dollar amount every year for as long as she lives).

Then Wendy bought a $5.6 million insurance policy (actually owned by an ILIT, so the death benefit will go to her kids tax-free). How are the premiums paid? The annuity payments are used to pay the premiums. We turned $2 million (which would have been subject to estate tax) into $5.6 million (tax-free) guaranteed. Awesome!

Example No. 4: Turning a tax disaster (qualified plan funds) into a tax victory.

Zelda (73) and Izzy (76) are married and worth $10.5 million, including $2,720,000 in a rollover IRA. We used a strategy called a "Retirement Plan Rescue" to purchase $5 million of second-to-die insurance (again, in an ILIT). The crazy American tax laws hit all qualified plans (including IRAs) with a double tax (income and estate). Here the double tax hit would be an astounding $1.66 million (using current tax rates), leaving the family with only $1.06 million … a tax tragedy. Using our strategy the family will get the full $5 million (free of all taxes). Cool!

Example No 5: You have an old policy and are no longer paying premiums out-of-pocket.

I saved the best for last. If you have a so called "paid-up-policy" (no longer writing checks to pay premiums), for sure you are getting ripped off. The insurance company will not tell you, and the agent who sold you the policy is just not doing his/her job. Either a single-life policy or a second-to-die policy can be the culprit.

What follows is a classic example: Alfred (71) had a policy with a death benefit of $4.2 million, with a CSV of $1.7 million. He no longer paid premiums because the annual earnings on the CSV was large enough to pay the premiums when due. Alfred was able to trade in the old policy (a tax-free transaction) for a new policy with a $7 million death benefit (using an ILIT again to make it all tax-free). Wow!

To give you an example of all the possibilities for using life insurance to increase your wealth without risk or increasing your current policy's death benefit without increasing premium cost, would take a huge book. So, I cornered my insurance guru and twisted his arm into agreeing to audit the insurance policies of readers of this column without any obligation. Or maybe you are just looking for a new policy to increase your current wealth without risk.

Either way, send me a fax (on your letterhead if in business) at 847-674-5299 along with a short note about your life insurance situation. Please include all of your phone numbers: business, cell and home. Write "Life Insurance" on your fax.

Irv Blackman, CPA and lawyer, is a retired founding partner of Blackman Kallick Bartelstein LLP and chairman emeritus of the New Century Bank, both in Chicago. He can be reached at 847-674-5295, e-mail [email protected], or on the Web at: WWW.TAXSECRETSOFTHEWEALTHY.COM.

About the Author

Irving L. Blackman

Irv Blackman, CPA and lawyer, is a retired partner of Blackman Kallick LLP and chairman emeritus of the New Century Bank, both in Chicago. He can be reached at 847/674-5295, via e-mail or on the Web at: www.taxsecretsofthewealthy.com.