The Wall Street business model is broken

Because this is a tax column, when readers call me to consult, taxes — usually concerning business transfer or estate planning — are at center stage. Most callers are business owners.

Can you guess what the most common request for non-tax help has been through the years and still is today? Hands down, it is how should I invest my personal funds, my IRA, my company's excess funds, and my company's pension plan, profit-sharing plans or 401(k). Often the funds belong to mom or dad, the kids, one or more trusts or an estate.

Most business owners complain, telling me that they don't have time to handle their own investments, their investments turn sour or they lose money, etc.

Since the drubbing the stock market (read Wall Street) took during the recent recession, callers, including my estate planning clients, are pleading for investment help. Sorry, this is not my skill. But their constant cries for help motivated me to try and determine if there is a logical, profitable and safe alternative to the current way Wall Street does business.

Current model

What I discovered about Wall Street startled even me. This is a tough subject. I am about to kill some sacred cows. Let's start by putting the current Wall Street business model on the table: The investor (Joe) buys a stock, bond or mutual fund. He pays a commission. If Joe has an investment advisor (Sam), he also pays Sam a management fee. This is OK with me if Sam delivers by having Joe's portfolio go up in value.

But wait… What if the value of Joe's portfolio goes down, way down, like 20%, 30%, even 40% or more? Everyone knows the sad answer: the same commissions and fees continue, increasing his losses. Can you name another industry or even one business that survives over time when it does not deliver its promised product or service?

How has this insane business model survived decade after decade? My research reveals the answer. Jim Shepherd, the author of the "Shepherd Investment Strategist," says it best:

"The media now calls the last ten years the 'lost decade.' But it did not seem lost as they reported… Instead, viewers [of TV, radio listeners and print readers] were hit with an unceasing litany of omission and positive spin, effectively coloring a gloomy economy consistently brighter, But why the spin?

"Because the media relies on advertisers… they must report the news in a manner that pleases the advertiser or the advertiser takes their business elsewhere… large brokerage houses… want investors to keep buying, or at least not sell stocks. The media is pressured to report financial releases as 'news' in as positive a manner as possible.

"Over the last decade, this positive spin met its purpose: it kept most investors in equities, even though equities lost almost 35% over ten years!"

This is bad enough, but even worse, my research revealed what should be a national scandal. Some quotes from an excellent article by Eleanor Laise, January 2009, titled "Big Slide in 401(k)s Spurs Calls for Change," exposed the scandalous story:

"About 50 million Americans have 401(k) plans, which have $2.5 trillion in total assets, estimates the Employee Benefit Research Institute… In the 12 months following the stock market peak in October 2007, more than $1 trillion worth of stock value held in 401(k)s and other "defined contribution" plans was wiped out…

"The most obvious pitfall…401(k) plans. Shift all retirement – planning risks – not saving enough, making poor investment choices – to untrained individuals, who don't have the time, inclination or know-how to manage [the risks]."

The plain fact is that the investment losses outlined above are the result of an invest-in-equities, buy-and-hold mentality.

To be thorough, my decision was to research traditional conservative investments. First, municipal bonds: A large number of reliable sources thought municipal bonds (and bonds in general) could be the next bubble about to break because interest rates are at an historic low. If (more likely when) rates go up as predicted, along with anticipated inflation, the value of bonds will plummet.

Any hope for other conservative investments? Well, take a deep breath and read what Kiplenger said in its November 2010 newsletter:

"Short-term interest rates are headed even lower… to zero on certificates of deposit with terms under 12 months as well as money market accounts. The average for CDs now 0.85% and likely to slip an additional 5 basis points a month… Money market accounts are typically paying even less, roughly half a percent."

Now we are ready for the good stuff… information that will help you recapture the profits of yesteryear. Let's start by looking back at how easy it was during the 1980s and 1990s to hire an investment advisor and get those delightful profitable results as the equity markets roared higher.

What changed?

As we entered the 21st century, the market switched from a bull market to a secular bear market. Secular bear markets are defined as periods of great volatility (drastic up and down price movements in stocks, indexes, mutual funds and other investments) of investment returns with little or no upward price movement, even though the trading range is large.

For example, say an index today is at 1,000. The index yo-yos back and forth over some period of time (it could be a week, month, year or more) within a range that reaches a high of 1,333 and a low of 691. At the end of the period (say two years) the index closes at 1015. A tiny 15 points up, a rise of only 1.5%.

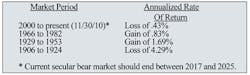

Such secular bear market periods last, based on market history, between 17-25 years on average. The following are the unhappy numbers of what actually happened during the last four secular bear markets with the S&P 500 stock index.

The lesson is clear: Buying and holding securities just does not work during secular bear markets. Can you make money during a secular bear market? Yes, but only if you have a proven plan that identifies when market conditions (related to your portfolio) clearly show a change in market direction may be coming.

Trend following

This is where the investment strategy known as "trend following" shines. This strategy does not attempt to predict market or stock movements. Instead, the strategy capitalizes on the natural market's movements (really the volatile ups and downs) whenever or wherever they occur. Trend following managers take advantage of what is actually happening in the market, rather than trying to guess what may happen in the future.

Trend following turns volatility from a foe into a friend. A trend is a strong, sustained move that can last from several days to a number of years. A trend may be rising or falling and is applicable to any specific security or index or a commodity (like oil, gold or the Euro).

How does a portfolio manager who is a trend follower make money? He waits for the market to develop a new trend and then invests with that trend, holding that position until there is a reversal. The manager does not invest at the exact bottom because he wants confirmation that a turn (reversal) has occurred. Likewise, the manager will generally not sell at the exact top, which is more easily identified after the fact. The manager will sell after a clearly identified change in trend (reversal). Therefore, the manager is able to capture 80%-90% of the trend.

What a great concept! You make money when the same investment trends up and make money again when it reverses and goes back down, then start all over again. Fine, I like it. But where do you find a trend-follower manager with a proven track record? Enter lady luck. I found a firm that has been using the trend following strategy since 2006. The results: Positive double-digit annual returns every year. And when the stock market crashed in 2008, their return was up over 23%! (Remember, prior results do not necessarily predict future results.)

An exciting fact: The system was designed and implemented by a portfolio manager hired by Sir John Templeton to manage a mutual fund in an advisory firm owned by Sir John's family. The portfolio manager also received a five-star rating for the last 10 years.

If you want to make a killing in the market, this strategy is not for you. However, if you want to shoot for a conservative, steady and proven return, you'll embrace the trend following system.

The SEC rules require that you (and your spouse combined) must be worth at least $1.5 million (including your home, IRA and other assets). Want more information? Send me (Irv) a fax to 847-674-5299 with your name, address and all phone numbers (business, home, cell) on your stationery if you own a business. Write "TREND FOLLOWING" at the top of your fax.

Irv Blackman, CPA and lawyer, is a retired founding partner of Blackman Kallick Bartelstein LLP and chairman emeritus of the New Century Bank, both in Chicago. He can be reached at 847-674-5295, e-mail [email protected], or on the Web at WWW.TAXSECRETSOFTHEWEALTHY.COM.

About the Author

Irving L. Blackman

Irv Blackman, CPA and lawyer, is a retired partner of Blackman Kallick LLP and chairman emeritus of the New Century Bank, both in Chicago. He can be reached at 847/674-5295, via e-mail or on the Web at: www.taxsecretsofthewealthy.com.