Lifetime plan will complete estate plan

Joe, a successful business owner at the age of 66, has been reading my tax column for over 20 years (he saves them in an ever-growing file). Recently, Joe read one of my columns about lifetime planning. It hit home.

Immediately, Joe e-mailed me telling a bit about his family, his business (Success Co.) and his current estate plan and a lot about his frustration — Joe was not comfortable with his estate plan.

I called Joe to talk to him and get more information. Joe agreed to send me a “consulting package,” which brought me up to speed on his current financial situation (both business and personal) and family. Included was a copy of his estate planning documents completed 15 years ago, but amended twice.

What was Joe’s estate plan? A typical A/B trust with his wife Mary (age 64) and an irrevocable life insurance trust (ILIT) that owned a $4 million whole life insurance policy on Joe.

In a classroom, the plan would get an A. Like most of the plans I review, the plan would be implemented when the client goes to heaven. Good! But the sad fact is that the typical A/B trust (like Joe’s and Mary’s and probably most married folks reading these words) cannot save you — or your spouse — even one dime in estate taxes.

Yes, an A/B trust, accompanied by a pour over will, is a good start. But burn this into your mind: such a trust, from a tax start point, is a loser — the IRS always wins. Your family loses.

The fact is Joe is a poster boy for a well-to-do business owner who can benefit — big time —from a lifetime plan to accompany his existing estate plan. The following is Joe’s current financial position, his current estate plan and the lifetime plan we created to beat up the IRS... legally.

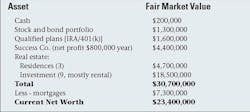

Below is Joe’s and Mary’s Financial Statement. Remember, over time mortgages will be paid off and the underlying real estate tends to increase in value.

Simply put, Joe’s taxable estate (net worth) will most likely significantly increase (to the $35 million range) and more than double the potential estate tax liability.

Joe agreed with the above analysis of his current estate plan. A few well-chosen expletives followed.

Joe’s & Mary’s Lifetime Plan

An estate-tax killing lifetime plan is asset based. Following are the various strategies that we used to reduce or eliminate the estate tax... for each significant asset (over $1 million).

Stock,bond portfolio: The entire portfolio was transferred to a family limited partnership (FLIP). Joe stays in control, but the FLIP allows us a 35% discount ($455,000) on the $1.3 million... estate tax savings of $182,000.

Qualified plans: We transferred the 401(k) funds into the IRA (a tax-free transaction). Then we used a strategy called a retirement plan rescue. Please note that funds in qualified plans are double taxed: income tax and estate tax. This strategy avoids the double tax (in the 64 percent range) and multiplies the after-tax dollars (all tax-free) via life insurance.

A lifetime plan can increase the wealth your family gets after you go to heaven.

In a nutshell, the IRA buys an annuity on Joe and Mary, then distributes the annual annuity payments to Joe. The after-tax annuity payments to Joe pay the premiums on a second-to-die policy on Joe and Mary (owned by an ILIT). The ILIT was able to buy $2.8 million of insurance. Result: We turned $96,000 (after-tax value of the IRA) into $2.8 million tax-free dollars.

Success Co.: We used an intentionally defective trust (IDT) to transfer (sell) Success Co. to one of Joe’s sons who was running the company. Joe keeps control (via owning 100 shares of voting stock), while he sold 10,000 shares of non-voting stock to the IDT. After discounts, the price of the non-voting stock is only $2.64 million.

The future cash flow of Success Co. is used to pay the $2.64 million. All the payments received by Joe (both principal and interest are tax-free). Not only does Joe stop the $800,000 annual income from increasing his wealth, but Success Co. is out of his estate.

Real estate residences: Joe sold one of the residences and kept the main residence and a summer home. We used a portion of their $5.45 million lifetime exclusion, because Joe and Mary want to keep those two residences for life.

Investment: All nine properties were already in LLCs owned by Joe. We transferred Joe’s interest in these LLCs to a second FLIP and sold the limited FLIP interests to a separate IDT. Result: We saved about $2.6 million in estate taxes because of the discount (about $6.5 million). Plus, the anticipated increase in real estate value is out of their estate. Joe said “Wow!”

Life Insurance: We were able to use the cash surrender value of the existing $4 million policy and continue the same premium amount to buy $6.5 million of second-to-die insurance. Result: an increase of $2.5 million in tax-free wealth, without any additional cost.

By now you get the idea. Almost 100 percent of the time a lifetime strategy can be used to a.) increase the value (usually tax-free) of each asset or b.) reduce the potential estate tax liability of that asset.

If your estate plan is already done, go back and take a look at how a lifetime plan can increase the wealth your family gets after you go to heaven.

Want to learn more... browse my website at www.taxsecretsofthewealthy.com. Got a question, then call me (Irv) at 847/674-5295. Or email me at [email protected].

Irv Blackman, CPA and lawyer, is a retired partner of Blackman Kallick LLP and chairman emeritus of the New Century Bank, both in Chicago. He can be reached at 847/674-5295, e-mail [email protected], or on the Web at: www.taxsecretsothewealthy.com.

About the Author

Irving L. Blackman

Irv Blackman, CPA and lawyer, is a retired partner of Blackman Kallick LLP and chairman emeritus of the New Century Bank, both in Chicago. He can be reached at 847/674-5295, via e-mail or on the Web at: www.taxsecretsofthewealthy.com.