2018 Insurance market outlook: What can you expect?

by JEFF CAVIGNAC, CPCU, RPLU, ARM

JAMES P. SCHABARUM II, CPCU, AFSB

PATRICK CASINELLI, RHU, REBC, CHRS

MATT NOONAN, CIC, RHU, CHRS, CCWS

For mechanical, electrical and plumbing contracting firms, insurance is one of the largest costs. When you add up premiums for Property, General Liability, Auto, Workers’ Compensation, Employee Benefits, Life Insurance and other lines of coverage, it can often total five percent of revenues or more. And that is only the direct costs. If you factor in the indirect costs, this number can more than double.

Due to the magnitude of these costs, it is critical to understand not only how to proactively manage them, but also how to forecast your costs as you look ahead to your next fiscal year.

In the long run, the only way to lower the cost of risk is to lower the frequency and severity of claims that drive the premiums as well as the indirect costs. In the near and intermediate future, however, you will also be affected by the insurance marketplace. The purpose of this article is to give some perspective on where the insurance industry is today and how the industry’s current finances and underwriting objectives might affect your business in 2018.

The insurance industry today

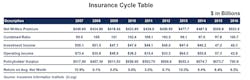

Table 1 shows that from 2008 to 2012, the industry’s “Return on Average Net Worth” was poor. This was attributable to a lousy combined ratio and a low level of investment return (the majority of an insurance company’s portfolio is invested in debt obligations; they can only invest about 20% in equities).

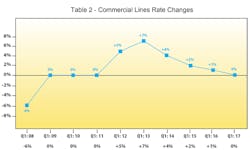

The industry needs to attract capital (surplus) to continue to grow. In order to do that, it needs to earn 10% or more in returns. When returns deteriorate like they did from 2008 to 2012, underwriters try to get more rate (increase premiums). This is reflected in the rate increases illustrated in Table 2.

The industry in 2013, 2014 and 2015 performed well, but not great. Insurers earned modest underwriting profits but decent overall returns. Rates in these years were flat and started trending down. This decrease in pricing adversely affected 2016 results. Insurance companies basically broke even on underwriting (combined ratio of 100.7%) and overall returns dropped from 8.4% to 6.2% — a 26% drop.

The first six months of 2017 continued the downward trend. The industry recently posted a $5.1 billion underwriting loss for the first six months of 2017 compared to a $2 billion loss in the same period last year. Net income year over year fell from $15.4 billion compared to $21.6 billion in 2016.

The industry will be further impacted by the devastating effects of the recent hurricanes. Hurricanes Harvey and Irma promise to be two of the worst national disasters to ever hit mankind and it is estimated that total damages could be as high as $100 billion. Insured losses could range $30-40 billion, although it is too early to have a precise amount. To put this in perspective, Katrina cost somewhere in the neighborhood of $176 billion, of which $82 billion was insured.

Overall the Property and Casualty insurance industry remains in pretty good shape and, although it does have its share of challenges, we are still projecting flat renewal rates with modest rate relief for preferred accounts. This, of course, will vary by line of coverage.

Allied lines

Allied Lines includes Property, General Liability, Auto and Umbrella. With the exception of Auto premiums, these lines should stay relatively flat. That does not mean that underwriters will not seek modest rate increases — they will. However, in most cases, rate increases can be negotiated. Auto is the exception. Auto experience has deteriorated recently, and it is estimated that State Farm lost over $7 billion on their auto book in 2016!

The deteriorating results are attributable to increased claims frequency (distracted driving) and increased severity. The increased severity is driven (no pun intended) by higher medical costs, which affect bodily injury claims and higher physical damage costs to repair damaged vehicles. The cost to fix a sensor and camera laden bumper today is a lot more than it cost to just replace the bumper 10 years ago. On top of that, it is estimated that over 500,000 vehicles have been destroyed by Hurricane Harvey alone, and flood damage is not excluded on most auto policies.

Contractors’ professional and pollution liability coverage

This line of coverage remains fairly competitive. Policy terms, however, differ widely by insurance company and alternatives need to be researched carefully. “Rectification” and “Mitigation of Loss” coverage should always be included but are not offered by all companies, and protective liability should also be part of the policy form.

It is also critical that the account be presented correctly to the underwriters. This can make a huge difference in the terms provided by an insurance company. Contractors Professional and Pollution Liability applications are long and can be confusing to complete. It is recommended that, prior to finalizing the application, you sit down with an experienced insurance broker who can explain the rationale and ramifications of each question.

Surety bonding

In 2018, the surety industry in the United States will continue to post further growth in overall premiums and below-average loss activity.

The total direct written premium for the calendar year end for 2016 was up to $5.88 billion from the prior 2015 year of $5.62 billion (a 4.5 percent increase). Impressively, at the same time the surety industry loss ratio fell in 2016 to 15.5 percent from 18.3 percent the previous year. This high watermark for surety industry volume continued to increase through the second quarter of 2017 to $3.13 billion in revenues with a 13.6 percent loss ratio (compared to $2.98 billion in revenues with an 18.4 percent loss ratio at the second quarter of 2016).

Strong growth and profitability since 2005 has attracted an increased number of new sureties to the market, creating fierce competition for market share. During the last five years alone, start-up frontline contract and/or commercial surety company operations have included AmTrust, Axis, Ironshore, Freedom Specialty, Allied World, Berkshire Hathaway, QBE, Euler Hermes, Navigators, Crum & Forster, Patriot, Endurance, Everest, Sirius, Markel and Argonaut.

Additionally, the number of surety re-insurance companies has almost doubled since 2008, from 17 to 32 (see Table 5). Although underwriting standards are relatively stable, overall supply has out-paced demand. This fresh credit capacity will cause further increased pressure to relax and soften terms and conditions (i.e., capacity, rate, indemnity, etc.) throughout the surety market.

The slow and steady economic growth has extended the current building cycle to a sluggish pace. This has also lengthened the surety industry’s positive historical results. Continuing labor shortages, inflation, interest rate hikes, and other factors will likely further slow the economic engines in the coming years.

Wise contractors are now getting margins, building their balance sheets and conserving for a rainy day. Contractors should begin positioning themselves for the impending shift ahead by retaining the best management team and labor talent; closely managing material, field and overhead costs; and demanding acceptable margins to ensure long-term success.

Executive risk

Executive Risk includes Directors & Officers (D&O) Liability, Employment Practices Liability (EPL) and Fiduciary Liability. The headache from the last economic downturn appears to be waning and these lines of coverage are reasonably competitive. Every form is different and there are a number of new players who may not be around in five years. On average, we are expecting flat renewal terms with some opportunities for rate relief.

Workers’ compensation

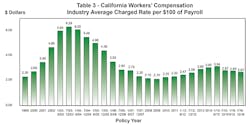

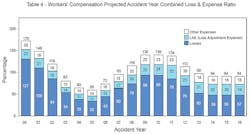

Workers’ Compensation experience in California has improved significantly since 2011 and rates on average have dropped 15 percent since the first half of 2015. The rate reductions are even more impressive when you look back to 2003 when the Average Charged Rate (ACR) was $6.29, as shown in Table 3. Through the first six months of 2017, the ACR in California is $2.58 (nearly a 60 percent decrease!) Since 2013, combined ratios for this line of coverage have been positive (under 100 percent) but losses are trending up and 2017 is likely to come in close to 100 percent, (see Table 4.) Despite this, rates have continued to trend downward. This, however, could change.

The Workers’ Compensation Insurance Rating Bureau (WCIRB) proposes Pure Premium Rates that are approved by the Insurance Commissioner. Every insurer then publishes its own rates. It is the average charged by all the insurers in the state that make up the Average Charged Rate.

The Bureau has submitted its January 1, 2018, pure premium rate filing to the California Department of Insurance proposing advisory pure premium rates that average $1.96 per $100 of payroll. This is slightly less than the current recommended pure premium rate of $2.00. The proposed decrease follows five consecutive advisory pure premium rate decreases since early 2015 that have totaled more than 27 percent.

Our projection is that rates in 2018 will, on average, be flat to down 5 percent. It is important to point out, however, that rate changes will vary by classification and by insurance company.

Health Insurance

The Affordable Care Act (ACA) is still the law. A number of “repeal and replace” bills have failed to pass, so the law will continue to be enforced. We are still waiting on information about the Cadillac Tax and whether regulations will be implemented.

For 2018, the number of age bands is likely to change. Currently, for small groups (2-99 employees), most insurance carriers have one rate for children under 20 years old. In 2018, insurance carriers will divide the 0-20 age group into seven bands: 0-14, 15, 16, 17, 18, 19 and 20. As a result, premiums for age 20 and below could see significant increases of 20-50 percent.

Rates for all “small” employers will be based on the employee’s and their dependents’ individual ages, plan design and location of the company. For example, a family of five will pay for each family member based on each individual’s age and the plan they select. Some younger employees or families with one child may realize lower premiums. All of the small group plans have changed to conform with the law and most have higher deductibles and copays; therefore, employees will have to pay more when they use the services.

The actuaries at all the major insurance companies have determined that, to stay in compliance with the ACA’s metallic tier guidelines, they must change plan benefits every year. The ACA guideline gave a percentage requirement for each tier – 90% = Platinum, 80% = Gold, 70% = Silver and 60% = Bronze. As costs increase, the value of the percentage changes and, therefore, the plan benefits change. Using the Platinum Plan as an example, if the actuarial value of a plan this year was $1,000, then the Platinum Plan has to cover 90% ($900) and pass 10% ($100) to the plan member. In the second year, if the actuarial value goes up to $1,100, 10% ($110) can be passed to the plan member and the benefits will change. This will always be a moving target until the values are fixed or the law is changed.

Wise contractors are now getting margins, building their balance sheets and conserving for a rainy day.

The provider networks are still changing and are offering a lower number of choices for doctors and medical groups. The industry calls them skinny networks. Often the price looks good, but your employees will have very few choices for doctors. Be sure to run a report to compare current providers to those associated with any programs you are considering. Insurance carriers continue to seek greater discounts from hospitals, medical groups and doctors and are offering patient exclusivity in return. Some insurance carriers will allow skinny networks to be offered side by side with full networks, with the price and contribution being set by the employer to favor one or the other. In 2018, businesses will see an overall 0 – 10 percent rate increase and benefit changes for “small” employers and 5-15 percent for “large” employers.

Captives, self-funding and partially self-funded plans are becoming more popular and should be considered for companies with more than 50 employees. Industry trust plans for all size of employers could lower the overall cost and stabilize the benefits. Other ways to reduce costs include buying a Bronze Level Plan and supplementing it with Cancer, Hospital, Accident and Critical Illness plans. Dental, Life, Vision and Disability continue to be very popular benefits with employees.

Conclusion

The insurance industry remains in a solid financial position. Despite the costs of the hurricanes, rates on average should be consistent, if not trending down slightly. The industry, however, has a good memory and has not forgotten the mediocre returns experienced from 2008 to 2012. Most underwriters still want more rate but the industry’s capacity (as measured by surplus) continues to have a downward effect on pricing.

While the health of the insurance market will directly affect what you pay for insurance, a much more important element is your Risk Profile. When an underwriter considers your account, they will evaluate your overall operations, your Human Resources practices, safety culture and overall safety practices, as well as your loss history.

A positive Risk Profile will result in substantially better pricing than a poor Risk Profile. This underscores the importance of proactively managing your cost of risk. The only way to lower your insurance premiums and the total cost of risk in the long run is to reduce the frequency and severity of the claims that drive this risk. While you cannot control the insurance marketplace, you can directly control your Risk Profile.

Cavignac, Schabarum, Casinelli and Noonan are principals of Cavignac & Associates, a leading risk management and commercial insurance brokerage firm providing a broad range of insurance and expertise to design and construction firms, as well as to law firms, real estate-related entities, manufacturing companies and the general business community. Founded in 1992, the firm currently employs a staff of more than 50 people at offices located at 450 B Street, Suite 1800, San Diego, Calif., 92101.